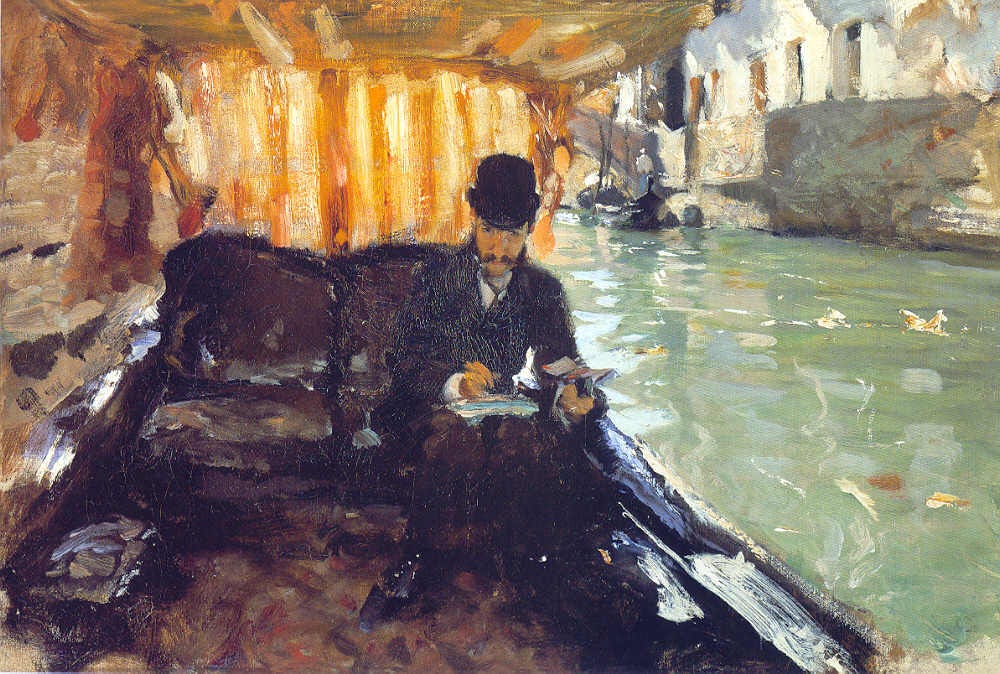

I didn’t expect to want to write a review as I walked down York Monday night to the M72 bus with a belly full of Trader Joe’s Pork Gyoza. My mind was mostly on a post in r/FoodNYC, soliciting recommendations for the best spot to score frozen dumplings in Chinatown. It seems Tasty Dumpling, where you can exchange $16 for 50 pieces, is the place.

I texted Max B if he had an opinion, looking to close the loop on my denunciations of disappointment regarding H, whom he’d met on Marathon Sunday. Getting my mind off her was a fairly substantial impetus for booking it crosstown to the Lincoln Square AMC for the 7:15 screening of Trier’s latest, which I’d sadly missed during the NYFF (I saw Peter Hujar’s Day, Father Mother Sister Brother, and the skinny Turkish girl who didn’t want to go on a second date because I took her to the Biancarnival).

I’d purposefully left my AirPods and my wired jawns at home. As I sat on the stagnant bus, parked low like a cat done a bun, I realized I felt connected to the world, to the City, to my fellow passengers, in a way that has been much much too rare in the past months. I looked down at my hands with their veiny protuberances. It was clear I was at ease, present, embodied, and open to receive this film from a director I so cherish.

Margaret Talbot, in her just-published profile of Joachim Trier for The New Yorker, calls the Norwegian auteur a “therapized man” and writes that he self-describes his directing style as one of “tender encouragement.”

As the movie ran in front of me, a feeling best described as Sehnsucht predominated.

Trier films are visual museums of Scandi-Germanic sensibilities, somewhat reducible to what the man glibly calls “nice light and colors.” Anders Danielsen Lie, the wonderful actor who plays only a small role as protagonist Nora’s married lover in Sentimental Value, describes the Trierian atmosphere as “walking through Oslo in June, early in the morning, coming home from a party, and the smell of the lilacs.”

Watching Sentimental Value, I had a million tiny flashbacks condensed into a singular moment that nonetheless lasted the length of the film. I saw myself shopping solo at German IKEA; trekking through the slushy streets of Kollwitzkiez for a professional lunch; standing in line at The Zig Zag with a joint and the unrequited love of my life; returning home after a beer with Hannes on the M10 schwarzfahren; straddling my DDR-era bicycle nach Grunewald; a post-Sisy Döner with a stranger from Bucharest; spontaneously running into friends on Türkenstraße in München; the time Pietro and I snuck into the awards gala for a public architecture competition in Zürich.

At the Zag during my mustache era. Fit goes quite hard tbh (not my unrequited love, that’s Rosa there)

At the time, of course, I was just in the arena, trying stuff. There wasn’t necessarily an intention to suffuse Germanic aesthetic characteristics into my person, accumulating like studded gems in a necklace. Even contemporaneously, as your classic dandy-pensive, I was not considering these implications; my mind was rather on pleasing an invisible audience, pursuing intrigues to keep their gaze fixed on me. But this is a topic for another day. Let’s get back to the review.

Trier’s overarching project seems to be the chronicling of dazzling horizontality.

Characters in Joachim Trier movies tend to share close similarities. They are depressed, they were gifted children, they are unsure of how to best apply themselves. They mostly direct their energies towards creating problems for themselves, in the absence of more base or primal scarcities. Modern Norway is a utopia, sort of. It has, in Talbot’s words, a “melancholy beauty…lush but empty-looking parks; [a] moody indigo fjord.” You can audition for drama school with whatever material you wish (as Nora does early on in Sentimental Value). You can then have stage fright and create problems for all of your co-workers, but it will be warmly forgiven and recognized as just a bout of eccentricity.

Or you can jump around in your mid-20s, starting on track to be a doctor, then a psychologist, and finally a photographer (see Worst Person) and your only real penalty is that you will have a comfy but unexciting job at a beautiful modern bookstore. The consequences of failure, of things not working out, are, in Trier’s films, often rendered in terms of emotional or psychic damage, rather than as tangible, worldly concerns.

Sentimental Value, to its credit, does go beyond this Trierian tendency by including the small plot point of Gustav’s mother’s role as a Nazi contra during the Second World War, though, even with images shown of torture techniques, the more resonant detail is that she never spoke about her time in internment to her family.

Industrious characters, like Aksel in Worst Person or Gustav in Sentimental Value, seem to undertake projects to burnish them in an array, rather than to accumulate them in a stack. There isn’t much of ‘I’ll do this, so then I can do this even harder thing’ but rather more of ‘this is the thing now and there will be a new thing later’. A healthy perspective? Probably. But one rather at odds with the realities of global competitive pressures.

Children, and the joy and hope they represent, are a recurring theme across Trier’s oeuvre. In Sentimental Value, Nora is very close to her nephew. At one point, they are snuggling under the covers and he declares that he will marry her as soon as he grows up, which, in a fantastically acted movie, delivers an apex moment as the anxiously-avoidant Nora laughingly enjoys the irony.

The extremely lovely and blushy Renate Reinsve as Nora

Trier’s heroes and heroines are consistently encountering examples of the bourgeoise settlement (kids, stable job often in the public/artistic sectors, etc.) and, more often than not, the dramatic tension of his films can be summed up by ‘how does x or y, in their pursuit of meaning outside of this compact, end up getting their knickers in a twist this time ‘round?’.

I’m not trying to be grouchy here; I am a huge fan and I believe quite firmly that this focus nails the Zeitgeist, especially in wealthy urban Europe. I’m writing this piece largely in response to my fellows in the crowd Monday night at the AMC Lincoln Square, who could be heard calling Sentimental Value “depressing” and “lacking a plot.”

If Trier’s Oslo is a place consumed by its horizontality, the United States, and Manhattan (but definitely not Brooklyn!), is pure vert. Energy should not be diffused horizontally, it needs to be concentrated, stacked, allocated; speaking should not be done for its own sake; it’s a quid pro quo, you validate my experience and I validate yours. There are always comparative advantages to be discovered, so we transact and make bets.

Thus, our culture, in stark contrast to the film, is all heroes journeys, aspiration, underdog story. Things go up, they go down. It’s the complete opposite of a diffuse, meditative European film. We like beginnings, endings, a clear conflict and a clean resolution. What it is is a masculine culture: direct, unsubtle, simple out of necessity.

So, yeah, of course there is no ‘plot’, as such. That’s the point. It’s how it feels, not what happens.

To wrap things up, I want to say a word about music. Trier’s a DJ too and his films are lovingly draped with tender bangers. I’d say his taste is very much NTS-coded, the London-based internet radio station that very well may be the true beating heart of contemporary European culture.

Trier’s filmography and the ‘auditory aesthetic’ of Dill’s program are unsurprisingly close, if not part and parcel. Flo is unabashedly left-wing, very much a Corbynite. It’s not difficult to imagine that some 90% of her listeners are the same. On a recent broadcast, she notes that no one in the chat is feeling better than an 8/10; for her part, she’s a mere 5/10. Everyone seems to want more of the world, yet few seem motivated to find it; they prefer to connect themselves to those, fictional or real, to whom they feel archetypally related.

I guess the métier is yearning. The music Flo plays, the situations Trier’s characters find themselves in: it’s basically a relentless torrent of unmet desire. What’s the prescription to lift these blues, though? Is it just a never-ending cycle of heartbreak? I don’t know, I guess it really depends on who you ask.

Anyways, I loved it. Very happy we live in a world that allows Mr. Trier to make his movies. 4.5/5.

Nothing lasts forever Of that I’m sure But now you’ve made an offer I’ll take some more Young loving may be oh so mean Will I still survive the same old scene?

I was born, raised, and educated close enough to capitalism’s pulsing core to grasp its logic, then spent my twenties deliberately far afield—immersing myself in Europe’s cultural ecosystems, learning to see American ambition from the outside, and developing the ability to translate between worlds that rarely understand each other. Now, I innately know how the game is played and have the hard-won ability to describe it with originality.

I grew up in Connecticut, in Westport, where I excelled in sports, went to Jewish summer camp, and read voraciously. By 15, I paid for subscriptions to the London Review of Books, The Economist, and The New Yorker with my umpiring money and annoyed my teachers by reading them surreptitiously in class. During free periods, I would go exercise at the Southport Racquet Club (now an Equinox) and chat macro in the steam room with retired day-traders.

At 18, I left home and went to Penn, where I discovered romantic longing and majored in Politics, Philosophy, and Economics with a side of German. A pivotal moment occurred in February 2017, my sophomore year, as I began to more seriously interrogate a future path in government/law. On the Amtrak back from Boston, after a final interview with the Mass. State AG, it dawned on me that I would go mad working under those drop ceiling tiles, in that stuffy government building on Commonwealth Ave, surrounded by kindly old ladies who’d been lifelong fonctionnaires.

So instead, I got in touch with these young guys who were building a simple screening tool for HR teams, out of the now-shuttered WeWork Gramercy on 23rd and Park, and my life in tech began. I joined a seed focused VC fund (where I first read Reaction Wheel!) the following summer, 2018, and they introduced me to a fund they knew based out of Berlin. After a few chats, we decided: I’d move to Germany directly after graduation and join their team from June 2019.

But things didn’t quite turn out that way. The German Consulate in New York denied my initial visa request, and then, a month before I was due to land in Germany’s capital, an appeal as well. The firm then withdrew their offer. Any rational person would have canceled the ticket, reconsidered, regrouped. Instead, I boarded the plane with a one-way ticket to a city halfway across the world in which I had no place to live, almost zero personal connections, and no immediate job prospects. But I was curious, and driven by a belief in my very core that things would work out for me if I showed conviction and created real value by being doggedly differentiated.

And thus I arrived May 29, 2019 in the city I would grow up in for a second time. I treated job-hunting like warfare—cold-emailed every fund in town, crashed every event I could find, memorized the faces of every partner in the ecosystem. Within weeks, I had an offer from one of the larger Berlin funds, focusing on Series A deals. In my eyes, Berlin promised me the chance to be a VC as soon as possible. But over time, something shifted–I became fascinated by the city’s peculiar relationship with ambition, with creativity, with the American dream refracted through a social democratic European lens.

It was also then that I started writing. I launched my Substack in December 2019 because I saw a gap: few voices were chronicling the European tech ecosystem, and even fewer from the perspective of someone who grew up in the American paradigm. I wanted to be a bridge between the continents, explaining to both sides what the other is really up to. I wrote weekly for three months, publishing essays that decoded Europe’s peculiar relationship with ambition, and added 300 subscribers in that time—a small audience, but one that actually read.

And then came COVID and a new job at one of Berlin’s great startup success stories, where I worked for 2.5 years. In this time, I began really living in Europe, absorbing its manners, observing its customs and taking part in its rituals (when I wasn’t locked down). I traveled widely, almost always on my own, intent on finding my way to the Zeitgeist, wherever I went and no matter who I encountered.

Poker games with minister’s sons in Paris, multi-day birthday parties in Austrian castles, meeting someone at the world’s most famous nightclub and spending the next five days together uninterrupted before saying goodbye forever. Pure creation, nothing inevitable, alles aus dem Nichts.

Professionally, I sought to better align the generative creativity of my explorative personal life with what I worked on in the daylight hours. So I joined a fintech company out of Paris to be their in-house industry evangelist and creative force.

There were some challenges, however. First, I came into the job under a cloud, heartbroken in a manner that still, three years later, makes for painful conjuring. Second, I had no real experience in embedded finance, the space I was meant to evangelize. And finally, we were creating content for an audience that didn’t know it was an audience. People wake up thinking ‘I’m a pilot’ or ‘I’m a nurse,’ but nobody, especially in Europe, wakes up thinking ‘I’m an embedded finance professional.’

The pay was good (for European standards) and the travels interesting so I continued, though I knew pretty well that I was defying my own nature and that time would eventually run its course. And so it did, in January 2024, when I asked to be released from my contract. Here is the best thing I wrote there.

By 2024, I’d become the American who could explain Europe to Americans and America to Europeans—a useful bridge but an exhausting middle. I was neither here nor there, too much of one thing and not enough of the other to truly be embraced by any one group.

The final episode of this story begins last summer, 2024. After a short visit back to the United States for my cousin Josh’s wedding, I returned to Berlin and began a romantic relationship with a woman I’d known during my university years, who was on an extended visit from New York. This injection from the past brought me to my senses: I was languishing in the ennui garden of Berlin.

Waiting for the S-Bahn one day at S Warschauer Straße, an idea ambushed me. I could build the kind of European ecosystem I’d long been agitating for by writing a new story--one that, in its telling, would require me to embody the cultural bridge I’d invested so much in becoming.

Inspired, I wrote my best and most successful piece yet. It was a public cover letter, similar to this one, making the case for a financial organization that sits in Europe’s heart and invests in fledgling European funds, yet imports capital and what I like to call ‘Silicon Valley Expansivism’ from the United States. The job, then, would require someone who could 1) deeply understand ‘tech propaganda‘ and localize its tenets for European understanding, 2) grasp the opportunity in Europe well enough to create a thesis for why it’s best to back emerging managers over established ones, and 3) sell the proposition in hard-to-navigate American capital markets (only possible as a native son/daughter).

I’d conceived of the perfect role for myself, and I knew exactly where I could prosecute it.

I’d known the GP of Multiple Capital for years. We’d connected over a shared sense of exclusion from the insular German VC scene, which we both found repugnantly conservative. He ran the best-known emerging manager fund of funds in Europe and had built a reputation as a contrarian voice on LinkedIn—someone willing to challenge the prevailing European narratives.

When I pitched him on joining Multiple, he agreed immediately. I’d raise capital in New York while building a content engine that would position the firm as Europe’s champion of tech optimism—finally becoming the bridge I’d spent five years preparing to be. My German citizenship application hinged on employment with a local concern; this felt like my last chance to make Berlin work, to prove the five-year bet had been worth it.

But early warning signs I’d ignored became impossible to dismiss. I’d structured an aggressive deal—earning a share of every dollar I raised—and built a compelling go-to-market strategy with the firm’s thoughtful and competent Principal over the first two months. I was preparing to stake my reputation in American capital markets on behalf of this firm and its thesis.

Yet the GP had built something I’d failed to see clearly: a fund whose small size and narrow niche insulated him from real competitive pressure. Years earlier, he’d turned down a €400k+ p.a. role at a Hamburg family office—more than his fund will generate in carry for over a decade. During the 2021 boom, Tiger Global had approached about an acquisition in the mid 8-figures—a chance to operate at real scale. He’d declined both. Not out of conviction in his model, but because he’d found a structure that let him operate on his own terms without the need to provide a superior product to beat out competitors.

I’d thought this was European conservatism I could help overcome. But it wasn’t conservatism—it was a fundamental asymmetry in how he viewed commitment. The GP expected total fealty while offering none in return. I was meant to spend my social capital arranging meetings with American LPs for someone who couldn’t show up on time, to sell a fund whose economics didn’t add up. The math didn’t work, the respect wasn’t mutual, and I wasn’t willing to burn my credibility on either front.

After two months, I resigned.

February...a brutal moment in Berlin during the best of times. As I circled the Lietzensee one stultifyingly cold day, watching my breath hang in the gray air while navigating the abundant black ice that rendered every step deliberate, I understood: I was free now. I no longer had to be the Berlin guy, living this life that frustrated me so. I could move toward something more aligned with my true desires: meaningful work, proximity to family, a stable domestic situation.

Dueling emotions boiled up in me. Relief flooded in–I could finally accept it was time to move on from this unfitting world. But also shame, disappointment that I’d foisted this false life onto myself. In truth, there hadn’t been much premeditation about moving abroad—I’d left behind the only context I’d ever known for a literal black box. It wasn’t ‘I’m doing this to ensure ideal conditions’ but rather ‘how cool would it be if I made this happen?’

And now, since June, that’s June 2025, I’m back in the States, living in a little studio in Yorkville, searching for the right opportunity to bring myself up to where I belong. I want to work with every fiber of my being, to embody a role and have the role embody me. My ability to gain access, to clock the situation and chameleonize, is indisputable.

My recent experience at the US Open is great proof. I worked the whole two weeks in the dessert kitchen making $19/hour, kicking it with my girls Fantasia, Essence, and Jessica from the block.

From left: Me, Nicole, Fantasia, Essence, Marielle, and Jessica at our station

With the Courtside Premier Crew after my promotion

Outside, the likelihood of us meeting would be close to 0%, with our interests, consumption patterns, educations so at odds. Yet in the kitchen, flattened by our drab uniforms and the dispensable nature of our positions, we got along well and smoothly developed mutual respect. And then, when my shift ended, I would go out onto the grounds or in the stadium, swiftly remove my uniform and stash it in the plastic bodega bag I always kept in the back-right pocket of my black Uniqlo slacks, don my sunglasses, and assume the more fitting role of Max as US Open spectator; kicking it with private equity CEOs, Instagram tastemakers, and startup middle managers.

Aye aye!

This is the skill I’ve been developing all along—not just the ability to code-switch, but to be genuinely present in radically different contexts without performing. It’s also, I realize, the essential skill of writing incisive profiles: to enter a founder’s orbit, understand their logic and dreams and fears, then translate that experience for readers who live in entirely different worlds. The writer as bridge. The writer as the insider’s outsider. The writer who’s equally comfortable in the dessert kitchen and the courtside seats, not because he’s pretending in either place, but because he’s learned to be himself everywhere.

Writing features for Colossus appeals for this very reason. No matter what, I’m going to find myself proximate to the economically and culturally powerful; it’s just who I am. In Europe, I focused on the culture, developing a read on the Berlin Zeitgeist that has few rivals in depth and scope.

Now I’m in New York, where capital and culture have become inseparable, where the most important stories of our time are being written by founders who are themselves trying to build new worlds. I want to chronicle that. I have the access, the curiosity, the hard-won ability to translate between contexts. What I need is the platform and the purpose. That’s what Colossus offers.

I’ve accomplished a lot without institutional support, compelled to justify my presence entirely through personal characteristics. Given the privilege of context, a clear raison d’être, and Colossus as a platform, I believe the pieces will come together naturally.

The story of John Singer Sargent is a story of light.

He was clearly a porous man, by that I mean one whose constitution allows the light to get in: highly sensible, an aesthete.

The exhibition itself is decidedly not structured chronologically. It is a study of Sargent’s discovery and subsequent use of light as the basis for a language of storytelling.

The first of his works to catch my eye was his Staircase in Capri (1878).

Staircase in Capri, 1878, Oil on canvas

Personally I was taken back to August 2021 when I visited the hermit village (it is accessible by only footpath or boat) of Loutro in Southern Crete. A time of mid-morning hikes along the coastal footpath that ended with triumphant swims in the quarter-boiled sea.

The view NE from the balcony of my hotel room. Note shadow on the wall to the left; that is where the staircase up to my room was.

There is no doubt, the light of the Mediterranean just hits different. And much of the effect comes from the verticality of the rugged shorelines, which cast unpredictable and polychromatic shadows.

It is not surprising, then, that Sargent’s studies of la luce caprese inaugurate the story of his artistic development. We see him first understand variations on luminescence as a method for the imbuing of character into inanimate objects. That gray fourth stair, the tri-angled shadow slowly revealing more of each ascending step, the foundational color of the many many whites. It’s not just a staircase, it’s a staircase of a particular place with its own stories and characteristics; the multiformity of its light and shadows gives it personality, windiness, a humane inconsistency.

Capri, 1878, Oil on canvas

It is difficult to see in this reproduction but once again Sargent’s dominant language is light. In the background, the mountains are shaded relative to the position of the Sun, which is the somewhat amusing white blob in the top-left corner. The dark blue in the bottom-left, which falls in the cleavage between a side of the building we don’t see and a shadowed valley below, does important work as contrast for the white building and the two figures in plein air.

It’s key that we as the viewer are slightly below the roof. We know then that the people are under the Sun’s full glory, spotlit, as if on a stage, where also their colors (pink, amber, navy) demarcate them as literally cut from a different cloth to their natural surrounds. Again, personality and character via Sargent’s handling of light.

Ramón Subercaseaux, c. 1880, Oil on canvas

Halfway through the vernissage now, I was struck by Sargent’s Ramón Subercaseaux (1880). The motive of light and color as the basis for Sargent’s approach to capturing his subjects’ essence becomes more obvious here. IRL, the water literally shimmers (just imagine the lighter patches popping), telling us perhaps what Sargent thinks of his friend the Chilean Counsel to Paris. The depiction of the Venetian boat is itself idiosyncratic, with an orgy of brown and orange hues that are giving expressionism, if not outright fantasy. Together with Subercaseaux’s attentive gaze, the environment of the boat reminds me of those precious moments of romance, often experienced in a drinking establishment, in which you are are almost certain you two are the only souls in the universe and the surrounds loses almost all their fineness.

Sulphur Match, 1882, Oil on canvas

Further along now, the outstanding Sulphur Match (1882) arrives. In contrast to many of the other displayed works, there is an obvious story here. The pair are drunk, perhaps the raven-haired girl even more so, with her feet perched like two seagulls on an invisible wire and, of course, her proximity to the upturned wine jug.

As an aside, the expression “non puoi avere la botte piena e la moglie ubriaca” entered my mind. Look it up if you wish.

Even with the obvious narrative elements, the clever deployment of shadow and light is vital to this painting’s success. The man, with his swarthy complexion and dark aura, looms as a bad influence, a tramp who has successfully cajoled the (perhaps only slightly more) virtuous maid into careless reverie. We don’t know where shadow ends and dude begins; it’s intriguing.

And now we finally turn to the main event: the portraits. But first a quote from Henry James:

“The highest result is achieved when to this element of quick perception a certain faculty of lingering reflection is added... the quality in the light of which the artist sees deep into his subject, undergoes it, absorbs it, discovers in it new things that were not on the surface, becomes patient with it, and almost reverent, and, in short, elevates and humanizes the technical problem."

Consider this before I show you the first of two paintings.

Sargent’s portraits are paragraphs, not statements.

Lady with the Rose (Charlotte Louise Burckhardt), 1882, Oil on canvas (Pardon the awkward crop, my picture)

My first reaction, after studying her face, was that she looked both German and American at the same time. As someone Who Would Know That, I turned out to be correct; Charlotte had a rich Swiss daddy and an American mom.

But what do we see in the face to give us that suggestion?

There is a certain insouciance, American, in her smile. I am hearing something like: “I am not impressed even though I know I don’t have the sophistication to have an opinion.”

Meanwhile, the Haltung is all German. It’s direct, it’s forward, it’s unambiguous while the necessity of having to perform any sort of gesture at all feels uncomfortable for the subject.

The shadow and light situation is just crazy. Observe the very top of the frame, the dancing patterns. And notice the floor with its three shades. The darkest shadow, the one behind and to her right, seems almost to have a personality of its own. It could be an avatar.

See also the background. Many gradients and shades, they are emotional cues for us.

The final work we will study is the one that made the biggest impression on me. I felt deeply moved by the dueling shades of blue, the modern countenance on Louise’s face, and the complex interplay of light between the foreground and background.

Madame Paul Escudier (Louise Lefevre), 1882, Oil on canvas

This is a complex and sensual woman. Our hint is the hands, suggesting one at peace with a truce made between the intellect and the soul. The shadows on her face deliver vital information. Her right side, behind her nose, is mostly dark save for a sliver under the eye. We are treated to Sargent’s interpretation of this remarkable woman, one who attracts a great deal of attention yet is almost impossible to know. A dramatic painting for a dramatic person.

What emerges is Sargent's gift that light does more than illuminate; it gives voice to the unutterable. His shadows whisper secrets, his highlights declare truths, and together they compose stories that words alone could never tell. This is portraiture as literature, written in the language of luminescence.

A great treat to see this exhibition, even with its final day crowds.

Note: This was written in May 2021. It was not initially published because Substack crashed and I lost a day's work, which has magically returned.

I have only made a few small edits and added a conclusion the day of publication (November 14 2024).

In the first section of the series, I briefly discussed the phenomenon that, in Europe, entrepreneurship is not given the same social cache as it is in the United States. While it has moved in a positive direction in recent years, this remains true today. Before we try to answer the “why” here, let’s look at “how” this manifests and the consequences of this on ecosystem growth and development.

Let Me Tell You a Story

For enterprising young people living in the Bay Area, the professional and social hierarchy looks something like this:

(Successful) Startup founders

VCs and angels

Investment Bankers, with TMT at the top

Startup operators

Corporate executives

Consultants

While many folks greatly admire the legends of investing, people like Doerr, Gurley and Moritz, it is ultimately the visionary founders who push young people to dream. This is even more true when it comes to the dynamics of the system itself.

Californians working in technology are uniquely attuned to the power of long-tail outcomes, asymmetric upside, and of storytelling to realize the levers of runaway success. Strong storytelling ability is required of all the occupations listed above, of course. That being said, I believe the Californian hierarchy rests on the centrality of storytelling ability to success. Americans have always recognized that a good story can function as an exponential multiplier and further, that order and certainty can negate such an advantageous mechanism.

Indeed, the United States was created as an idea, a story waiting to be told.

Let’s look at the role of storytelling in the hierarchy above:

Storytelling ability is an important trait of a consultant. The consultant must tell the story of a particular decision. They must understand the context behind why a decision must be made, who the decisionmakers are, and what kind of consequences the decision may lead to. But, ultimately, the leverage the skillful storyteller consultant enjoys does not extend past the decision-level.

Storytelling ability is an important trait of a corporate executive. The executive must tell the story of her firm’s stock price. They must understand the context behind the recent performance of the stock price, who, amongst stakeholders, is most responsible for its performance, and what can be done in the next quarter to improve it. But, again, the leverage of the adroit storyteller exec doesn’t affect anything more than the company’s stock price.

Storytelling ability is an important trait of a startup operator. The operator must tell the story of the function they are responsible for. They must understand why their function can be a growth driver for the business, who should be on the function’s team, and what the fundamental business value of the function’s activities is. The leverage of the wise operator applies only to their function, where it logically ends.

Storytelling ability is an important trait of an investment banker. The banker must tell the story of their advisee’s IPO or acquisition. They must understand why the business is an attractive place for investors’ money, who the important leaders of the advisee are, and what synergies/advantages can be unlocked from the transaction. A banker that can tell stories well can make the difference between a successful transaction and one that flounders, but their influence does not extend past this single event in the firm’s lifespan.

This section in table format, if that’s more your thing

Storytelling ability is an important trait of a venture capitalist. The VC must tell the story of the financing round. They must understand why the startup should take their money over others, who they can introduce the startup to for hiring or sales purposes, and what growth the financing can accelerate for the company. A VC will not win the deal if they are unable to adequately story tell, which is their raison d’etre, but, as with the banker, a way with words has consequences for the singular event but does not quite extend to true value creation.

Storytelling ability is the most important trait of an entrepreneur. The founder must tell the story of the entire company. They must understand why the company can win in the space, who can dream and execute the company into existence, and what the impact on society the company can make. Strength in storytelling is non-negotiable for a startup founder and will make-or-break the success of the project.

In my view, the single most important question a founder can ask themselves when they are deciding to build a business is: can I tell stories effectively? Perhaps the brilliance of Northern California as an entrepreneurial ecosystem is that there are so many opportunities to flex this muscle and proficiency is highly valued by all ecosystem participants.

Not a Care in der Welt

As Alex Danco writes in his instant classic, Social Capital in Silicon Valley, the region’s ecosystem is designed to reward those who transact, leverage, and tell stories with their innate social capital because it signals that one could, down the line, create tremendous value out of invested financial capital. Danco says it best:

“For a young founder in Silicon Valley, your social status is the most valuable thing you have: not only because it can open doors for you, but also because using your social status effectively is like a dress rehearsal for raising money and making deals. If you can demonstrate to early prospects and investors that you’re successfully able to promote hyped-up equity in your own reputation, it’s a good sign that you’ll be able to successfully sell hyped-up equity in your startup too. This is that special sort of magic quality that hangs around some founders like a halo. You instinctively know what they’re capable of, because at a social level, you’ve already seen them do it.”

Don’t get me wrong. This phenomenon exists in Europe. In fact, it is much more prevalent now than it has ever been. But it just doesn’t function in the same way. The biggest reason, I think, is that people just don’t care really. If you work in tech in SF or NYC or Miami, whether in Customer Success, Marketing or Backend Development, it is expected that, for the most part, you are following the trends, gossip, and news of the day. Further, there is a large group of operators, investors and founders who spend a lot of time being clued in, deeply invested in ecosystem-shaping narratives and their outcomes.

In Berlin, and I assume London too, this is just not happening at the same scale. What you have instead is a small (I mean a few dozen, not thousands) group of investors and founders who, in Germany at least, often attend the same universities, have previous experience in consulting and are usually white men who grew up relatively well-off (more on this later) who care a lot, and then like 95% of the ecosystem not giving a single shit about anything outside their own positions and companies. The reasons for this are quite interesting.

In big European hubs, startup workers come from all over the world, often motivated by quality of life concerns. At Choco alone, I have colleagues from Brazil, China and Nigeria. They don’t know who Sebastian Pollok is. They never will, even though he is one of our investors and also the husband of a fellow (now former) colleague. They’re simply pleased to work at a great company with an inspiring mission in one of the most livable cities in Europe. On top of this, for those who might be from continental Europe and thus pre-disposed to being more in-tune with ‘The Scene’, they are also not engaged. The expected value, or relative upside, from investing time and energy into ecosystem development for most people is negligible. This is mostly due to a very conservative approach to equity-based compensation (driven by regulation), though this is shifting quickly. What I am getting at is there is basically zero inter-mingling in the tech industry here between labor and capital. Capital has made the decision that it will commit itself to ‘The Scene’ as a Lebensfokus. Labor is only in the most remote sense aware there even is a scene.

Aus dem Weg, Geringverdiener!

Returning to Danco, he introduces this amazing concept of “The Social Fog of War”. Basically, the premise is that the best-run systems enjoy an unintuitive advantage: they are illegible and opaque. Folks have a vague idea of who is on top and who is on bottom, but the closer you get to the middle, the harder it is to place yourself relative to others. Uncertainty is the gasoline to the fire here. And awareness will suffocate the flame. To quote Danco:

“If everyone suddenly became aware [sic] each other’s relative status, it’d be a social disaster: the group would collapse. The people on the bottom half will be made aware of their inferiority: they’ll feel self-conscious, like impostors. And the people in the top half will become aware of their superiority – they’ll feel pressure to break off from the group, which is obviously bringing them down. Ignorance was bliss.”

Uncertainty is not the friend of the European, even one with far higher than normal risk tolerance. Credentials are hunted and then zealously guarded.

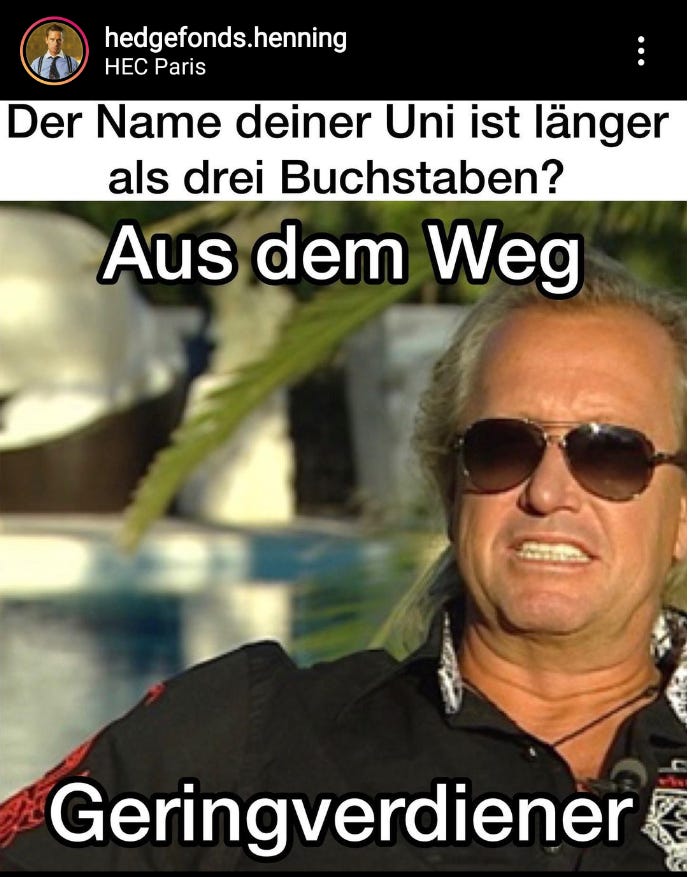

The phenomenon of credential-obsession stood out to me almost immediately after I moved to Berlin two (now more than five) years ago. As I was researching the venture landscape, I kept encountering rather young-looking people with these confounding LinkedIn headlines full of unfamiliar acronyms. Imagine my surprise when it turns out young, entrepreneurial (they are always so entrepreneurial) people in Germany are the most passionate credential hunters out there. Below, I have collected just a few headlines of people who liked a post celebrating the promotion of a connection of mine at a well-known, but not necessarily beloved, German seed stage VC a few weeks back. As an aside, seeing this type of thing in America is exceptionally rare. In all, these come from eight people.

Collected LinkedIn headlines of eight German twenty-somethings

There is a German finance Instagram account, quite similar to @litquidity, which made a wonderful meme lampooning what you see above. I think it makes my point better than anything I could write.

“The name of your university is longer than three letters? Out of the way, low (wage) earner!”

Second, as this phenomenon is quite well-spread, it serves to reason that leaders at venture capital firms react favorably to this kind of behavior. Funnily enough, I did an analysis of this myself on a cold, rainy day in Mallorca back in early March (big ups to #teamgoodlife).

I looked at the 35 non-partner investors, from Principal to Analyst, who were, at the time, employed by the ‘top’ 8 VC funds that expressly cover and identify with German-speaking Europe (DACH). While the proportion of female investment team members is slightly higher (23%) than individuals of any sex with a migrant background (17%), what I particularly found fascinating was the mix of the most relevant previous experience amongst this group. Over 25% of junior VCs in Germany have had their most relevant prior experience take place at a MBB consulting firm.

Experience 1 = most recent job

Now, I don’t know what this number looks like amongst junior investors in the United States but I’d be willing to bet that the share of those whose most relevant prior experience to working in venture was at a MBB firm does not exceed 10% and is probably around 5%. It is meaningfully significant for a junior VC to have spent time getting credentialed at one of the top global consulting firms in Germany. Echoing part one of this series, those involved in technology investing in Germany are unlikely to have significant operating experience, even amongst recent, junior hires.

In interviews with European investors, I have been asked multiple times something along the lines of, “which investors in *insert city* are the best in your opinion?”. Crazy! Literally grasping for order and hierarchy!

Danco warns against this, explaining that a shared understanding of social hierarchies disrupts the game theory away from productive collaboration:

“But when status becomes more codified and explicit, then the social capital of the entire group gets threatened. Clarity and order tilt the game theory away from the communal group and towards less productive posturing and gatekeeping. This is why so many startup incubator programs, mentorship programs, and support networks fail so abysmally. The formal roles, titles and milestones that they impose, even if individually sensible, break the illegibility and inclusion.”

This lack of respect for the power of disorder extends outside of the tech niche, of course. Returning to the hierarchy of occupations from earlier, this is what it looks like in Europe, from my vantage point:

Consultants

Corporate Executives

VCs

Investment Bankers

Startup Founders

Startup Employees

What’s the theme? Well, the role of the consultant, at least from the perspective of the client, is to provide certainty. Even if confidence in the path taken to certainty is low, the advisor must posture that he has reasoned with a clear and unobscured mind. The customer rents the certainty of the consultant and its firm to make decisions ‘on a more even footing’. Large-company executives must do the same for shareholders, employees, and customers alike. The more you rise up the chain of command, the less disorder is welcome. The consequence of all this is that entrepreneurs in Europe must navigate a world wholly un-designed for their needs.

While in California, where the “Social Fog of War” usefully limits the need for distracting posturing and status seeking, the European founder needs to work 2x as hard to succeed because they are probably not in the ‘in-group’ and are not granted the same benefits as those innovators in more supportive, opaque, and disordered systems.

To finish off this section, I just want to bring this all back to the investor side of things. Everett Randle, of Founders’ Fund, published a widely-read piece recently on how and why Tiger Global and other high velocity hedge funds are eating more traditional technology investors’ lunch.

My favorite part comes towards the end, where he likens Tiger Global (and other peer funds) to Walmart in their approach to selling the capital they have. By focusing on tremendous scale and velocity in their process, they will (really, already have) become the cheap option for startups when they need to purchase growth equity investment. You won’t get the bespoke design or customer experience, but you will get what you need, fast, without fuss, and reliably.

On the other hand, the funds with known brands and/or best-in-class vertical expertise that can be leveraged to ‘help’ portfolio companies, will sell a more expensive product, attractive to early-stage founders who need the credible signals on offer. He compares this approach to luxury brands like Tiffany & Co.

Randle worries for the J.C. Penneys, those investors who don’t have a strong brand nor the desire/willingness to innovate and embrace the (uncertain) realities of an evolving landscape. He thinks they will end up in a “Dead Zone”.

In 2021, there are quite a lot of J.C. Penneys in Europe. Sometimes it is because of LPs, who are even less keen on disorder and certainty than conservative venture capitalists. Indeed, to run Tiger’s playbook, you need extraordinary buy-in from capital providers. But many other cases are self-imposed. I know of a Series A focused fund that refused to seriously consider businesses that produce ARR below a fully arbitrary threshold. Or another that has had a rule for years stipulating that investment team members must hold a Master’s degree.

These nudniks will not survive in the long-term. And that’s probably a good thing for the ecosystem as a whole.

Wrapping it up

I was finally moved to publish this piece after seeing Aadi Vadiya post similar thoughts some 3.5 years later. It would surprise no one that nothing really has changed in this time. Old habits die hard.

I believe local VCs in Berlin actually have done some introspection and are aware of the deficiencies of the ecosystem they have developed. The problem is they don’t care to fix it because they get paid anyways. Their incentives are not aligned to deliver outcomes that benefit society.

The only way to change this system that is doing tragically little to arrest Europe’s decline is to swap out its players. As I have written previously, it is time for a new generation of investors to emerge, one that is unconnected to the cynical legacy of Rocket Internet, one that is made up of genuine technologists rather than erstwhile consultants, one whose financial success is tied to outcomes that deliver competitiveness and productivity gains for the continent.

If anything has changed since 2021, it is that entrepreneurs are increasingly deciding to found their companies in jurisdictions that do more to support them. They’re voting with their feet; it’s yet another reason we must do what we can to enact change.

At the beginning of my time in Berlin, indeed around when I wrote this piece, I really admired Germany and appreciated how its systems were so rife with local characteristics. But I have evolved on this front. These tendencies are limiting potential and positioning the ecosystem as uncompetitive. We need to embrace the rather American-coded power of storytelling to make sense of uncertainty and opacity while still retaining that herrliches collective spirit.

I think we can do it. But we really gotta push for it!

We arrived shortly before 8:00 PM. The line to get in easily overflowed out of the RAW Gelände and onto Revalerstraße, where it snaked along the Plakat-laden wall towards the Warschauer corner before it 180’d and began to ran parallel to itself back towards the venue.

Julius, Marco, Leti, and I were there already at the Wendepunkt, eating Döners almost lustfully. Marco, in his off-season, indulged in two.

In Berlin wohn’ ich, also steh’ ich an. I live in Berlin, therefore I queue.

It is impossible to separate the experience of waiting in a line with the reality of making the German Hauptstadt your home. The principle is straightforward enough: most everything is accessible, regardless of your income or status, as long as you wait your turn.

This inherent promise has a meaningful and perhaps underrated effect on the mentality of Berliners. Many believe that their responsibility is simply to show up and they will subsequently get taken care of. Implicitly, showing any kind of initiative more than this will be ignored.

I call this the Deli Counter Mentality and I think it is bad. But I will talk about this another time.

As we edged closer to the entrance, we were joined by Niklas and Moritz. They could not have timed their arrival any better, hitting us at the moment of ingress. The stars were aligning and the excitement inside was palpable.

It was my first visit to the Astra Kulturhaus and I was impressed by the venue. Almost twice the size of Kreuzberg’s better known Gretchen, the space delivers a comfortable vastness and proved quickly to be easily navigable.

Admittedly, my previous exposure to Ezra Collective’s music was rather limited. I know them mostly from the vital South London Jazz compilation We Out Here (2018), in which the group’s track Pure Shade is the “other song” to Kokoroko’s enormous Abusey Junction, which was a mainstay of undergraduate toking sessions at Fauxm and Mulch.

I am rather a fan of the group’s keyboardist Joe Armon-Jones, who closed out XJAZZ! back in May here in Berlin. The light touch of Armon-Jones’ keyboard playing is for me the most compelling element of the group’s sound. His introduction on Pure Shade, where he plays in counterpoint to woody percussion, demonstrates this nicely, as did a warming solo performed 2/3 through last night’s show; a pleasant dose of tenderness amongst a flurry of pulsing, urgent beats.

Interpretations of pop music numbers made up around a fifth of yesterdays concert. Angie Stone’s Wish I Didn’t Miss You was one such track and def a highlight. In general, I liked them, the crowd too. I told Julius in the moment that I appreciated the group doing so because it places them ‘in the tradition’ of the jazz masters of the mid-century, who famously selected popular songs from Broadway luminaries like Rodgers & Hammerstein, such as All the Things You Are and Embraceable You, to develop their own sound on top of.

The funny thing was that we easily identified the melodies but none of us actually could remember the titles of the tracks (Julius got the Angie Stone one later on). In fairness, we often pride ourselves on the obscurity of the music we like, so perhaps not a surprise there.

Regarding the band’s sound. Ezra Collective is not shy about its many influences. While it calls itself a jazz band, the influence of afrobeat looms large (they did an homage to Fela Kuti that was clearly the highlight of the concert for the assembled).

Focusing on the rhythm section, drums and bass, contemporary hip hop’s influence, think Kendrick Lamar, is substantial. Here, the connection to jazz fusion of the 70s and 80s, Herbie Hancock or Joe Zawinul’s Weather Report, is almost non-existent. Even though they are fundamentally a jazz fusion group, they sound more like a composite of afrobeat and hip hop than the next generation of fusion. I say this neutrally.

The band is after producing a particular music-going experience, one where movement and rhythm is at its very core. Today, the paying public is clearly looking for a more holistic experience when they approach jazz. This is why Ezra Collective can fill the 1,500 capacity Astra Kulturhaus while the brilliant Immanuel Wilkins Quartet performs in venues like the wonderful yet comparatively tiny Zig Zag, capacity some 200.

Final note on the band’s sound. I would say it comes together better as a marketable product than it does as a musical concept, much like the American (revivalist) jam band Goose, who I saw this summer in New Haven, Connecticut.

It seems, albeit from my somewhat limited concert going experience, that groups who claim a long list of influences are in vogue today. Perhaps a symbol of “stuck culture”, the recipe for commercial viability, let alone success, might very well be to unambiguously select a few successful genres from the recent past, blend them, and deliver a concert-going experience high on excitement and movement that is also referential enough to attract fans from the existing genres.

To sum it up: the innovation is more in the construction of a better customer experience than it is a step forward musically. The Immanuel Wilkins’ of the world, who, to me, are pushing the genre forward by crafting a fundamentally new and improved sound, are thus confined to smaller venues where the physical excitement quotient is more limited. But of course, it might just also be my taste talking here.

Credit: Julius Hoffman

I also must cover the political aspect of Ezra Collective’s performance, especially as it reminded me of frequent collaborator and fellow South Londoner Nubya Garcia, who performed in November 2021 at Gretchen.

Around halfway through, the Collective’s leader Femi Koleoso took the mic. He started by psyching up the crowd before quickly turning into a different direction. Koleoso proclaimed proudly that his band’s fundamentally cheery music is “not happy music” but rather is born out of darkness, a darkness that impregnates the whole world with its diabolical intent. After riffing for a few minutes on the darkness’ greatness and insurmountability, the crowd was starting to waver in enthusiasm. As a final flourish, the Collective’s leader constructed a juxtaposition, where joy exists as a counterweight to this ubiquitous darkness that pervades our world. The message was clear: there is no joy without darkness.

I won’t get into my view on the appropriateness of using the stage as a pulpit. I trust the reader will figure it out anyways. I rather discuss the view of the world Koleoso and his Collective aligns itself with.

The idea that there must be darkness for there to be joy should be easily rejected. Joy can very well exist and blossom on its own; it is not zero-sum. A joyful approach to life is one that centers on an expansive state of mind where optimism and a belief in a better future end up self-reinforcing themselves until they become true. Whether there is darkness, who’s experiencing it, and which groups ‘deserve’ it more or less don’t factor in here. Rather, such exercises tend to be zero-sum and usually don’t end up being helpful when it comes to taking action.

Giorgia Meloni had a solid observation in a recent speech she gave in New York. She revealed a central paradox of contemporary Western culture: we look down on ourselves while simultaneously feeling superior to other cultures.

The activism of Ezra Collective largely echoes this unfortunate paradox. Any joy we might have must first be qualified by acknowledging the darkness around it (looking down on ourselves). And then, we create a sense of superiority by congratulating ourselves for our own awareness of this ‘truth’.

With music, I am definitely in agreement that the contrast between sad and happy (usually sad lyrics and happy music) often makes for a thrilling result. Just look at Pet Sounds, this Michael Jackson song, or Blind.

But I am not sold that this is an effective method for creating an abundant joy that can benefit everyone. It seems rather to beget an unproductive navel-gazing that crushes the spirit, both collective and individual. Hopefully, I am wrong.

It was surprising that the band didn’t play an encore. It seemed clear to me that it was a political choice. No free labor. I am not sure what to think of that.

Thank you to my dear friends Julius, Letizia, Marco, Moritz, Niklas, and Pauli for a wonderful evening.